Click here to get this post in PDF

A credit score is a numerical expression based on a level of analysis of a person’s credit files, to represent the creditworthiness of an individual. A credit score is primarily based on credit report information typically sourced from credit bureaus.

The history of credit scores can be traced back early 19th century when commercial trade started expanding rapidly. At that time, businesses were looking for ways to determine which new applicants were likely to become good customers. This eventually led to the development of early credit scores.

The first real use of credit scores came in the mid-20th century when FICO (Fair Isaac Corporation) started using them to help lenders decide whether to approve loan applications. FICO scores are now the most widely used credit scores in the world.

The Basics of Credit Scoring

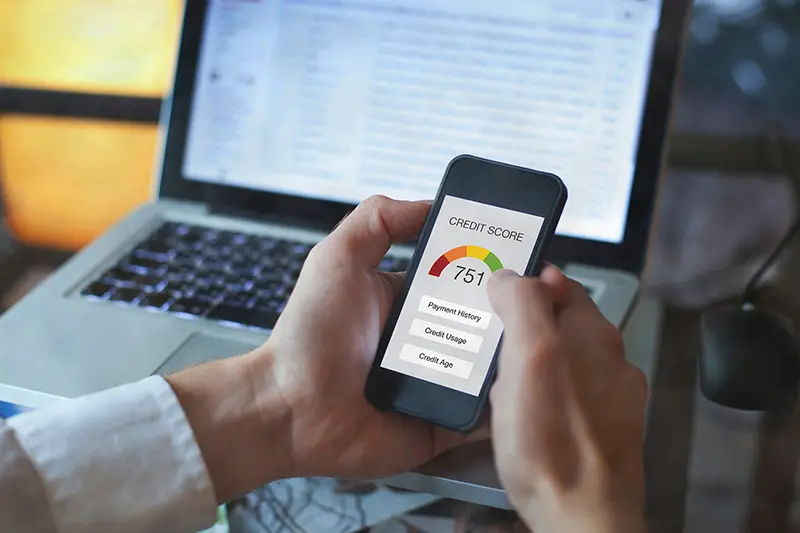

Most credit scores – including the FICO score and VantageScore – operate on a range from 300 to 850. A good credit score is typically one that is 650 or higher.

The actual scoring process is complex and often proprietary, but there are some basics that can help you understand how your score is determined.

Generally, your credit score is based on five main factors:

- Payment history (35%): Do you pay your bills on time?

- Credit utilisation (30%): How much of your available credit are you using?

- Length of credit history (15%): How long have you been using credit?

- Credit mix (10%): Do you have a variety of types of credit, such as revolving credit and instalment loans?

- New credit (10%): Have you applied for any new credit products recently?

These are not the only factors that can affect your credit score, but they are the most important ones.

Credit Scores Around the World

While credit scores are used all over the world, there are some differences in how they work from country to country. Here’s a look at how credit scores work in a few other countries.

The United Kingdom

Credit Reference Agency (CRA) scores keep records of an individual’s credit history and make this information available to businesses on request. The main CRAs in the UK are Equifax, Experian, and Callcredit.

There are no universal credit scoring models in the UK – each organisation has its own way of calculating scores. However, they all consider similar factors, such as credit utilisation, payment history, and length of credit history.

Scores in the UK typically range from 0 to 999, with higher scores indicating a lower risk of default.

Australia

Credit scoring in Australia is very similar to credit scoring in the UK. There are three main credit reporting agencies in Australia: Equifax, Experian, and illion (formerly Dun & Bradstreet).

The most widely used scoring system is the Comprehensive Credit Reporting (CCR) system. Under this system, credit reporting agencies must share positive information (such as on-time payments) as well as negative information (such as late payments) with businesses on request.

Scores in Australia typically range from 0 to 1200, with higher scores showing a lower risk of default.

The United States

In the United States, there are three main credit reporting agencies (CRAs) – Equifax, Experian, and TransUnion. These agencies collect information on your credit history and use it to generate your credit score.

The most widely used credit score in the US is the FICO score, which ranges from 300 to 850. A score of 700 or above is good, while a score of 800 or above is considered excellent.

Canada

In Canada, credit scores are called Credit Reporting Scores (CRS). The two main credit reporting agencies in Canada are Equifax and TransUnion.

Like in the US, the most widely used credit score in Canada is the FICO score. However, the range for a FICO score in Canada is different than it is in the US – it goes from 300 to 900 instead of 300 to 850.

Germany

In Germany, credit scoring is called Schufa, which translates to “Protection Association for General Credit Security.” Schufa is a private company that collects information on an individual’s credit history and makes it available to businesses on request.

Scores in Germany typically range from 0 to 100, with higher scores indicating a lower risk of default.

France

In France, there are no universal credit scores. However, bank lending decisions are often based on an individual’s “bank score.” This is a score that is calculated by the bank itself, using information from the applicant’s credit report. These data aren’t shared with other banks or businesses.

The Bottom Line

Credit scoring works differently all over the world, but the basics are the same – your score is based on your credit history, and it is used to assess your risk of defaulting on a loan. Keep these things in mind, and you’ll be on your way to a good credit score no matter where you live.

You may also like: Benefits of a Good Business Credit Score