Click here to get this post in PDF

Navigating the Regulatory Landscape of Financial Compliance and Recovery

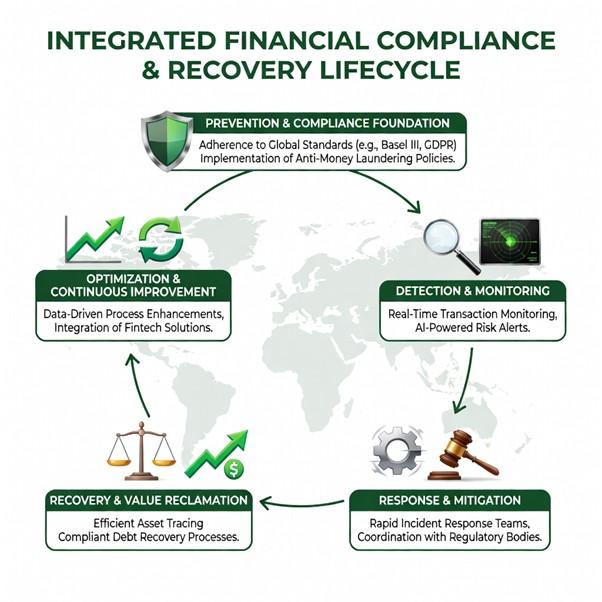

The modern financial landscape is dynamic and increasingly complex. For businesses today, strategic financial management demands more than just balancing the books. It requires a keen understanding of Financial Compliance and Recovery. These are not mere administrative tasks; they are foundational pillars for sustained growth and resilience.

We recognize that navigating regulatory challenges and safeguarding financial health is paramount. This guide will explore how robust compliance frameworks help businesses operate ethically and efficiently. We will also examine effective recovery strategies that protect assets and reclaim value.

We will delve into critical aspects, including core regulations and global standards, as well as advanced recovery planning and technological solutions. We will also touch upon ethical practices in debt collection, demonstrating how diligent ERC financial compliance recovery efforts, for example, are vital for reclaiming eligible funds while adhering to all necessary guidelines. We aim to provide a comprehensive overview that empowers modern businesses to build strong, compliant financial operations.

The financial sector operates under an intricate web of regulations designed to protect consumers, maintain market integrity, and prevent systemic risks. For any business involved in financial activities, understanding and adhering to these rules is not just a legal obligation but a strategic imperative. The cost of non-compliance can be astronomical, ranging from hefty fines and reputational damage to severe enforcement actions. In fact, compliance costs have surged by 60% for retail and corporate banks compared to pre-financial crisis spending levels, highlighting the growing complexity and importance of this area. Conversely, firms with robust compliance frameworks report 40% fewer regulatory interventions, underscoring the tangible benefits of proactive adherence.

In the realm of debt collection and recovery, specific regulations dictate how businesses interact with consumers. In the U.S., the Telephone Consumer Protection Act (TCPA) governs automated calls and texts and requires consent for certain communications. The Servicemembers Civil Relief Act (SCRA) provides protections for active-duty military personnel, impacting interest rates and collection actions. The Fair Debt Collection Practices Act (FDCPA) sets strict guidelines for third-party debt collectors, prohibiting abusive or deceptive practices. These regulations are just a few examples of the dense regulatory environment that requires constant vigilance.

Federal Oversight and SLFRF Reporting Requirements

For entities receiving federal assistance, such as the State and Local Fiscal Recovery Funds (SLFRF), compliance monitoring is particularly stringent. The U.S. Treasury has made it clear that it intends to vigorously monitor how recipients obligate funds, especially following the December 31, 2024, obligation deadline. This commitment includes recouping funds that violate SLFRF rules.

Recipients must be acutely aware of their reporting obligations and deadlines. For instance, Annual and Q1 Project & Expenditure (P&E) Reports are typically due on April 3, 2026, with updated user guides and compliance resources available from the Treasury. These reports detail how funds are being spent and obligated, ensuring transparency and accountability. To assist recipients, the Treasury provides comprehensive Compliance and Reporting Guidance(Updated October 2025) and various tools, including webinars and simplified portal demonstrations. Adhering to these guidelines is crucial to avoid potential fund recoupment and ensure the proper use of public resources.

Global Data Privacy and Cybersecurity Standards

Beyond specific collection practices, broader financial compliance regulations protect sensitive data and ensure operational resilience. The financial services industry is a prime target for cyberattacks, making robust cybersecurity and data privacy frameworks non-negotiable. The average cost of a single data breach in the financial sector is a staggering $5.72 million, with a record 12,195 confirmed data breaches reported last year.

Globally, the General Data Protection Regulation (GDPR) in the EU has set a precedent for data privacy, influencing regulations worldwide. Violators of GDPR face severe penalties, including fines of up to €20 million or 4% of their annual global turnover, whichever is higher. Many global businesses adopt GDPR standards across their operations to streamline compliance.

In the U.S., regulations like the Gramm-Leach-Bliley Act (GLBA) require financial institutions to explain their information-sharing practices to customers and safeguard sensitive data. GLBA mandates the protection of “nonpublic personal information” (NPI), which includes a broad range of customer data. The Payment Card Industry Data Security Standard (PCI DSS) is another critical framework, a set of security standards designed to protect cardholder data. PCI DSS includes six goals and twelve security requirements for handling cardholder information securely.

The Sarbanes-Oxley Act (SOX), enacted after major corporate accounting scandals, primarily focuses on the accuracy and reliability of financial reporting. While not exclusively a cybersecurity law, SOX requires organizations to implement internal controls over financial data, particularly under Section 404. Similarly, the NYDFS Cybersecurity Regulation (23 NYCRR Part 500) mandates comprehensive cybersecurity programs for financial institutions operating in New York, including risk assessments, penetration testing, and incident response plans. The New York State Department of Financial Services (NYDFS) even announced new guidance in October 2024 to address cybersecurity risks associated with artificial intelligence.

More recently, the Digital Operational Resilience Act (DORA) went into effect across the EU in January 2025. DORA standards aim to enhance the digital operational resilience and security of the EU’s financial services sector by mitigating risks posed by third-party ICT vendors. These regulations collectively underscore the need for a proactive, comprehensive approach to data security and operational resilience.

Advanced Recovery Planning and Resolution Frameworks

For large financial institutions, particularly those supervised by the Office of the Comptroller of the Currency (OCC), recovery planning is a critical component of maintaining safety and soundness. Recovery planning is distinct from resolution planning, though both aim to manage financial distress. Recovery plans are developed by banks themselves to ensure their continued viability as a “going concern” during periods of severe stress, without relying on extraordinary government support.

The OCC’s guidelines for Recovery Planning, outlined in 12 CFR 30, Appendix E, mandate that covered banks establish robust frameworks to identify, measure, monitor, and control risks that could threaten their financial viability. These guidelines apply to large national banks and federal savings associations with average total consolidated assets of $100 billion or more, a threshold updated in response to recent bank failures to encompass a broader range of institutions.

Triggers and Stress Scenarios for Covered Banks

A cornerstone of effective recovery planning is identifying triggers and stress scenarios. Triggers are specific quantitative or qualitative indicators that signal a bank is approaching or experiencing severe financial distress. Quantitative triggers might include drops in capital ratios, liquidity levels falling below certain thresholds, or significant increases in non-performing assets. Qualitative indicators could involve negative media coverage, credit rating downgrades, or adverse regulatory actions.

Covered banks must include a range of stress scenarios in their plans, encompassing both idiosyncratic events (specific to the institution, such as a major operational failure or a rogue-trading incident) and market-wide events (such as a severe economic recession, a significant market shock, or a widespread cyberattack). These scenarios help test the efficacy of recovery options and ensure the bank can respond to diverse threats. Banks also employ reverse stress testing, which involves identifying scenarios that would lead to the bank’s failure and then working backward to understand the vulnerabilities and potential triggers. The goal is to calibrate triggers as leading indicators, allowing for timely action before regulatory minimums are breached.

Distinguishing Recovery from Resolution Planning

While both recovery and resolution planning address financial instability, their objectives and assumptions differ fundamentally. Recovery planning is an internal bank process focused on restoring the institution to a sound financial condition as a going concern. It assumes the bank will continue to operate and details actions it can take internally to overcome stress, such as capital injections, asset sales, or expense reductions. The emphasis is on maintaining financial viability and market confidence.

Resolution planning, on the other hand, is developed by regulatory authorities (like the FDIC in the U.S.) for institutions deemed “too big to fail” or systemically important. It outlines how a failing institution could be wound down in an orderly manner without causing broader financial instability or relying on taxpayer bailouts. Resolution planning explicitly assumes the bank has failed and cannot recover on its own.

In the context of recovery, regulators like the FDIC also have powers to impose restitution and civil money penalties (CMPs) on institutions and individuals who violate banking laws. Restitution is remedial, aiming to compensate harmed parties or disgorge unjust enrichment. CMPs are punitive, paid to the U.S. Treasury to deter misconduct. The FDIC uses a structured approach, including quantitative scoring matrices, to determine appropriate penalties.

Feature Restitution Civil Money Penalties (CMPs) Purpose Compensate harmed parties; disgorge unjust enrichment Punish misconduct; deter future violations Recipient Harmed parties or institution U.S. Treasury Nature Remedial Punitive Grounds Unjust enrichment or reckless disregard Violations, unsafe practices, breaches of fiduciary duty Tiers (for CMPs) N/A Tier 1 (violations), Tier 2 (patterns/reckless), Tier 3 (knowing substantial harm) Example Returning funds to customers overcharged Fines for AML failures or deceptive practices The FDIC’s Chapter 9 guidance on “Restitution and Civil Money Penalties” details the criteria for imposing these measures. For instance, Tier 3 CMPs are reserved for knowing violations or practices that cause substantial loss to the institution or significant gain to the individual. When resources are limited, the FDIC often prioritizes restitution to harmed parties over CMPs, ensuring that those who suffered losses are compensated first.

Operationalizing Compliance in Debt Recovery and Collections

Effective debt recovery and collections are crucial for financial institutions, but they must be conducted within a strict framework of compliance and ethical considerations. The Financial Conduct Authority (FCA) in the UK, for example, has significantly transformed debt recovery practices, with regulatory fines for breaches averaging £2.3 million per case in 2024. A staggering 67% of consumer complaints involve unfair debt collection practices, underscoring the need for a compassionate, compliant approach.

This is where agencies focused on protecting financial compliance and recovery play a vital role, ensuring that collection efforts align with regulatory requirements and ethical standards. Such partners help navigate the complexities of consumer protection laws while maximizing recovery rates.

Best Practices for Financial Compliance and Recovery in Debt Collection

To operationalize compliance, financial institutions must embed best practices into every stage of their debt recovery process:

- Treating Customers Fairly (TCF): This principle, particularly emphasized by the FCA, means communicating clearly, honestly, and without undue pressure. It involves offering realistic payment arrangements and ensuring customer understanding.

- Proactive Bankruptcy Monitoring: Staying ahead of bankruptcy filings is critical. Systems should provide automated alerts for events such as filings, automatic stays, dismissals, and discharges. This allows collectors to immediately cease contact when an automatic stay is in effect, preventing violations and potential legal action.

- Military Status Verification: Compliance with the SCRA requires identifying active-duty military personnel. This ensures they receive statutory protections, such as reduced interest rates and special collection account treatment, thereby avoiding penalties for non-compliance.

- Deceased Consumer Handling: Identifying deceased consumers proactively, before any contact attempts, is essential for ethical recovery. Automated notifications and verification processes help prevent distressing communications to grieving families.

- Right-Party Contact (TCPA Compliance): Utilizing sophisticated data and analytics to ensure contact is made with the correct individual, at the correct number, is paramount. Consumers change addresses, phone numbers, and emails faster than ever, and outdated information increases the risk of illegal contact under regulations like the TCPA, leading to potential damages and fines.

Supporting Vulnerable Customers and Ethical Recovery

A key aspect of modern financial compliance, particularly in debt recovery, is the identification and support of vulnerable customers. Regulators expect firms to have robust processes in place to recognize vulnerability and adapt their approach accordingly.

- Vulnerability Assessment: This involves monitoring indicators such as financial stress signals (e.g., missed payments, requests for payment holidays), health issues (physical or mental), recent life events (e.g., bereavement, job loss), or other circumstances that could impair a customer’s ability to make informed decisions or manage their debts.

- Tailored Support Plans: Once a vulnerability is identified, collection activities should be paused, and a thorough assessment conducted. This leads to the development of tailored support plans, which might include extended payment terms, reduced contact, signposting to debt advice services, or even debt write-offs in extreme cases. For example, a customer struggling with mental health issues might receive extended terms and reduced, empathetic contact.

- Proportionate Actions: Collection actions must be proportionate to the debt amount and the customer’s circumstances. An escalation matrix should guide actions, ensuring that aggressive tactics are reserved for appropriate situations and never used when vulnerability is present. For instance, initial contact for a small debt should be gentle, escalating only gradually and with due consideration for the customer’s situation.

Embedding these practices not only ensures regulatory compliance but also builds trust, protects the firm’s reputation, and aligns with broader ethical standards in financial services.

Technology and Third-Party Risk Management

In the face of escalating regulatory complexity and the persistent threat of cyberattacks, technology has become an indispensable ally in financial compliance and recovery. Three-quarters of banks and credit unions have embarked on digital transformation initiatives, recognizing that traditional methods are no longer sufficient. The sheer volume of data and the speed of financial transactions demand automated, intelligent solutions.

AI-powered monitoring, for instance, can detect anomalies and potential compliance breaches in real-time, far surpassing the capabilities of manual oversight. This proactive approach is crucial, especially given the record-high 12,195 confirmed data breaches last year. Beyond detection, technology streamlines regulatory reporting, which can be a significant cost driver. Compliance costs are up 60% for retail and corporate banks over pre-financial crisis spending levels, and automating these processes can lead to substantial savings and fewer errors.

The Future of Financial Compliance and Recovery Technology

The evolution of financial compliance and recovery is inextricably linked to technological advancements:

- AI and Machine Learning (ML): These technologies are revolutionizing compliance by enabling real-time risk detection, predictive analytics for fraud prevention, and intelligent automation of routine tasks like transaction monitoring and regulatory reporting. They help integrate siloed data to provide a holistic view of risk across an organization.

- Blockchain: While still emerging, blockchain technology holds promise for enhancing transparency, security, and immutability of financial records, potentially simplifying audit trails and cross-border compliance.

- Enhanced Cybersecurity: Beyond basic firewalls, advanced cybersecurity measures are critical. This includes robust encryption, such as the Advanced Encryption Standard (AES) with a minimum 128-bit key, and multifactor authentication (MFA) to protect access to sensitive systems. Aligning cybersecurity strategies with frameworks like NIST (National Institute of Standards and Technology) provides a benchmark for best practices.

- ESG Reporting Tools: With increasing regulatory focus on Environmental, Social, and Governance (ESG) factors, technology is vital for collecting, analyzing, and reporting on vast amounts of ESG data across the value chain.

Strengthening Governance and Board Oversight

While technology provides powerful tools, it must be supported by strong governance and active board oversight. A robust Compliance Management System (CMS) is essential, integrating policies, procedures, and controls across the organization.

- Internal Audits and Training: Regular internal audits ensure compliance frameworks function as intended. Continuous training for all employees, from frontline staff to senior management, is crucial to fostering a culture of compliance and keeping pace with evolving regulations.

- Third-Party Risk Management: Financial institutions increasingly rely on third-party vendors for critical services. This introduces significant risk, as vendors can become the weakest link in the security chain. Comprehensive due diligence, ongoing monitoring, and contractual agreements that mandate adherence to security and compliance standards are vital. When vendors experience data breaches, the financial institution can often be held accountable.

- Fractional Compliance Counsel: For many businesses, particularly those that do not require a full-time Chief Compliance Officer, fractional compliance counsel offers access to top-tier expertise without the overhead. These specialized services can guide regulatory interpretation, risk assessments, and policy development, ensuring that even smaller entities can maintain high standards of compliance and recovery readiness.

Frequently Asked Questions about Financial Compliance and Recovery

What is the difference between recovery planning and resolution planning?

Recovery planning is an internal process for a financial institution to restore its financial health and viability as a “going concern” during severe stress, using its own resources and actions. It aims to prevent failure. Resolution planning, on the other hand, is developed by regulatory authorities (e.g., FDIC) for failing institutions, outlining how they can be wound down in an orderly manner without causing systemic disruption or relying on government bailouts. It assumes failure and focuses on minimizing its impact.

How can financial institutions identify and support vulnerable customers during debt recovery?

Financial institutions can identify vulnerable customers by monitoring indicators such as financial stress signals (e.g., missed payments, requests for payment holidays), health issues (physical or mental), recent life events (e.g., bereavement, job loss), or other circumstances that might impair their ability to manage debt. Once identified, institutions should pause collection activities, conduct a thorough assessment, and develop tailored support plans. These plans might include offering extended payment terms, reducing contact, signposting to debt advice services, or considering debt write-offs, always prioritizing fair treatment and ethical engagement.

What are the key reporting deadlines for Treasury SLFRF fund recipients?

For recipients of State and Local Fiscal Recovery Funds (SLFRF), the obligation deadline was December 31, 2024. Following this, recipients must submit Project & Expenditure (P&E) Reports. For Annual and Q1 reporters, these reports are typically due on April 3, 2026. The U.S. Treasury provides specific guidance, user manuals, and webinars to help recipients meet these deadlines and ensure accurate reporting. Failure to comply can lead to vigorous monitoring and potential recoupment of funds.

Conclusion

Strategic financial management in today’s complex environment demands an integrated approach to financial compliance and recovery. By proactively navigating the regulatory landscape, implementing advanced recovery planning, operationalizing ethical debt collection practices, and leveraging cutting-edge technology, businesses can build resilience. This commitment to robust frameworks and ongoing oversight not only mitigates risks and avoids costly penalties but also fosters trust with customers and stakeholders. A strong foundation in financial compliance and recovery is not just about adhering to rules; it’s about securing sustainable growth and creating long-term value in an ever-evolving global economy.

Also read: What Businesses Need to Know About Financial Management

{kind=link}